China Investment in Africa: More of the Same?

Chinese financing trends in Africa, in the wake of the triennial Forum for China-Africa Cooperation. We weigh up the threat of “debt-trap diplomacy” on the continent, and highlight potential concerns regarding social, environmental and corruption issues associated with Chinese investment.

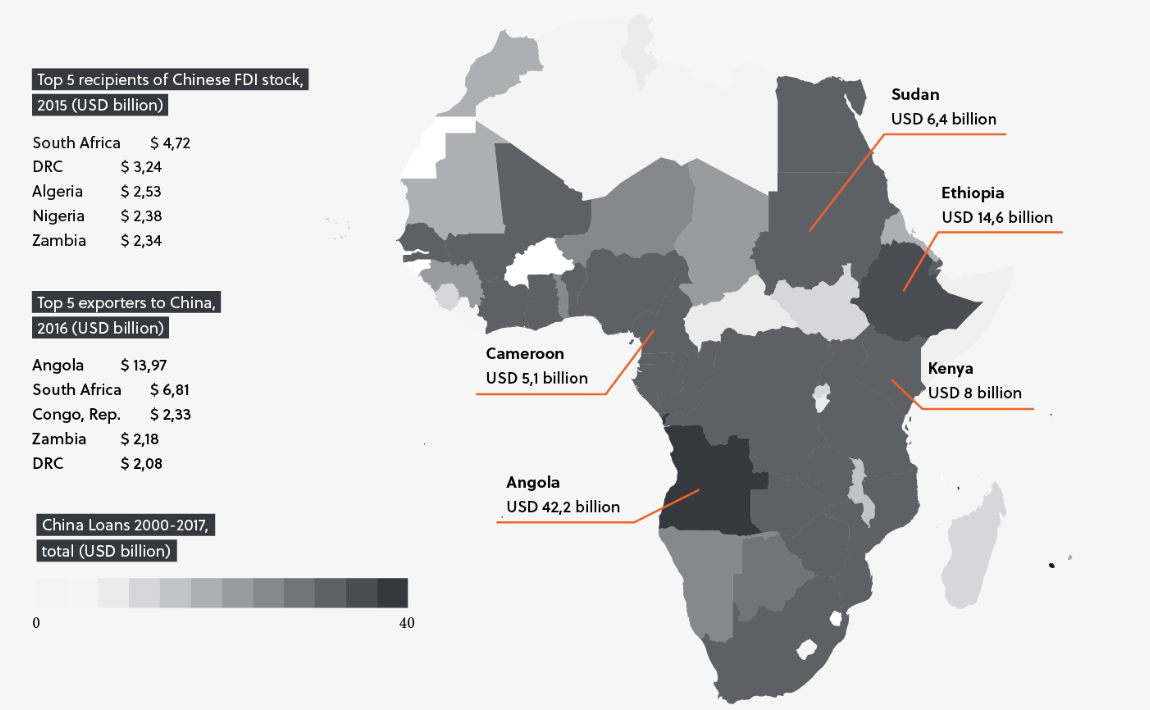

THE SHAPE OF CHINESE FINANCE

To date, Chinese policy banks – the China Development Bank and Export-Import Bank of China – have spearheaded the campaign via loans to African governments and state-owned entities, turning China into sub-Saharan Africa’s largest creditor with an estimated 14 percent of the region’s debt stock, excluding South Africa. The focus of this debt finance has been on addressing the region’s substantial infrastructure deficit – a trend which has seen the gross annual revenue of Chinese construction contracts in Africa increase from $1 billion to $55 billion between 2000 and 2015.

China’s trade with Africa has also expanded significantly – fed by Chinese demand for fuel, metals and minerals – with the country becoming sub-Saharan Africa’s largest export destination over the past decade. Foreign direct investment (FDI) from China has grown from a small base, to make the country the fourth largest FDI provider to the continent after the US, UK and France.

The main recent driver behind the substantial increase in Chinese finance into Africa has been Beijing’s Belt and Road Initiative (BRI), introduced by Xi Jinping in 2013. The BRI is aimed at improving access to foreign markets and resources by investing heavily in land and sea infrastructure projects across the Middle East, Asia, Europe and Africa. Initially focussed on East Africa, the BRI’s scope within the continent has expanded. A diplomatic tour by Xi Jinping in August marked this clearly – with Senegal becoming the first west African government to sign up to the BRI, and Rwanda, South Africa and Mauritius also featuring on the Chinese president’s itinerary, and receiving major funding commitments in his wake.

DEBT-TRAP DIPLOMACY

Increased Chinese engagement with the continent has not been without its critics. China has been accused of engaging in “debt-trap diplomacy”, whereby loans are traded for political influence and strategic assets. The example of the Hambantota Port in Sri Lanka is frequently raised. In 2017, China took control of the port after Sri Lanka was unable to repay the debts owed to Chinese banks. Government officials from the US, India, and Japan have since raised concerns that part of the port may be used a naval base.

The concern would appear particularly relevant to Africa, following recent IMF reporting that two fifths of low-income countries in Africa are facing a debt crisis. In Djibouti, where China holds over 80 percent of external debt, these concerns appear to have substance. The government received a $590 million loan from the Export-Import Bank of China in 2015 to build a port and, in 2017, China built its first overseas military base on an adjacent site. The US’s only Africa-located military base, Camp Lemonnier, is 11 kilometres from the port. The building of the port and subsequent Chinese military base has led to concerns among the US foreign policy community that Camp Lemonnier could be handed over to China and the US military ejected from the country if Djibouti is unable to pay its debts – several senators wrote to the US National Security Advisor in May, flagging these concerns, which they argued were made real by Djiboutian president Ismail Omar Guelleh’s failure to respect the rule of law, and his willingness “to sell his country to the highest bidder”.

A wider look shows, however, that Djibouti appears to be more the exception than the rule. According to research by the China-Africa Research Initiative at Johns Hopkins University, of 17 African countries in, or at high risk of, debt distress, China is the main contributor of debt to only three – Djibouti, Republic of the Congo, and Zambia.

GOVERNANCE CONCERNS

Governance concerns associated with Chinese financing are generally more valid. Chinese banks are not bound by the investment criteria of the Organization for Economic Cooperation and Development (OECD) – which has set the bar for environmental and social considerations by other major investors into Africa. The largest recipient of Chinese loans in the 21st century has been Angola, whose government has only recently attempted to reform its reputation for corruption (see next article). Chinese infrastructure loans are also peculiarly susceptible to contract inflation, as a result of the finance being tied to the use of specified contractors. Recent billion-dollar loans from Chinese lenders to fund a Kenyan railway and a South African state-owned transport company have been accompanied by accusations of high-level corruption.

Chinese financiers are increasingly cognisant of the need to address such concerns, not least due to their desire to court US companies as partners in BRI projects. This year’s FOCAC was notable for its overtures to the model of Western development finance in Africa, with a declaration of intent to diversify African economies away from an over-dependence on the extractives sector, and to encourage greater FDI from Chinese companies in Africa. Equally encouraging, Chinese banks have recently drafted sustainability criteria aimed at matching those of the World Bank. It appears China is attempting to replace its burgeoning – if not wholly deserved – reputation as an exploitative rent-seeker in Africa with that of a mutually beneficial business partner. Policymakers and investors alike will wait cautiously by, assessing whether there is substance behind the intent.