New Frontiers: The Changing Face of Conflict and Competition

Editor

While more traditional armed conflicts such as the Russia-Ukraine war remain major challenges for regional security, the evolving dynamics of warfare and state-sponsored terrorism has also driven changes in the risk landscape to governments and businesses. In an increasingly fragmented geopolitical environment, major powers are expanding the range of tools used to pursue national security goals, strengthen economic influence, and securing strategic resources. Throughout 2025, this shift has been reflected in intensified Russian grey-zone activity in Europe, more assertive military posturing and regional security measures in areas such as the Caribbean, and increased competition over strategic resources and critical supply chains.

These dynamics illustrate how geopolitical competition is carrying wider implications for businesses operating amid conditions of continued uncertainty in 2026.

State-sponsored terrorism: Grey-zone tactics

Grey‑zone activity (hostile actions that stop short of full‑scale war) has become an increasingly prominent strategy employed by states such as Iran and Russia to pressure and destabilise rivals. Notably, amid the Russia-Ukraine war, this has included efforts to destabilise rival governments, and leverage the cyber landscape to disrupt infrastructure, elections and public trust. Suspected Russian operations have involved physical sabotage, such as explosions damaging railway lines on the Warsaw-Lublin corridor in November 2025, which Poland’s government described as an “unprecedented” act of state‑linked sabotage against a route critical for aid to Ukraine. European security services have also linked a series of parcel fires in July 2024 at logistics hubs in Germany, Poland, and the UK to a Russian military intelligence plot to place incendiary devices in air cargo. Prosecutors said the devices were likely test runs for attacks on cargo flights bound for the US and Canada. In addition, there has been constant GPS‑signal jamming targeting air traffic over the Baltic Sea, with Sweden logging 733 incidents affecting civil aviation by late August 2025, up from just 55 in 2023.

Outlook

Russia has expanded its grey‑zone campaign against European NATO members over the past two years to not only deter continued military support for Ukraine, but also to weaken the alliance’s cohesion. From the Kremlin’s perspective, Russia is already in confrontation with the West, viewing NATO’s expansion and support for Kyiv as evidence of persistent hostility. Therefore, even if the conflict in Ukraine ends in 2026, grey‑zone activity in Europe is unlikely to subside. European leaders and NATO officials, including NATO Secretary General Mark Rutte, are increasingly framing these tactics as state-sponsored terrorism, with governments warning that continued grey-zone attacks could trigger tighter sanctions on Russia and pledging to strengthen security in areas such as undersea infrastructure and air and maritime policing.

As European governments work to counter this evolving threat, companies with operations or staff in Europe increasingly need to plan for disruptions not only on land but also in key maritime and cyber domains. Hotspots to watch through 2026 include the Baltic and North seas, where critical undersea cables and energy pipelines have already suffered damage, as well as the rail and logistics routes carrying military aid across Poland and the Baltic states. Companies operating in front‑line or strongly pro‑Ukraine countries – spanning defence, transport, logistics, energy, and

National security: Shifting priorities

The Russia-Ukraine war and broader geopolitical tensions have in recent years affected a shift in major powers’ security priorities, with ripple effects for traditional alliances, defence and economic agendas, and regional security.

This dynamic has had a significant impact on Europe’s response to Russia’s ongoing aggression. In June, all European NATO members except Spain pledged to raise defence spending to five percent of GDP, up from the current two percent target. This shift has largely been driven by sustained US pressure for greater burden sharing, prompting leaders in European capitals to present higher defence outlays and capability development not only as a response to Russia, but also as a hedge against uncertainty over the future scale and reliability of Washington’s military presence in Europe.

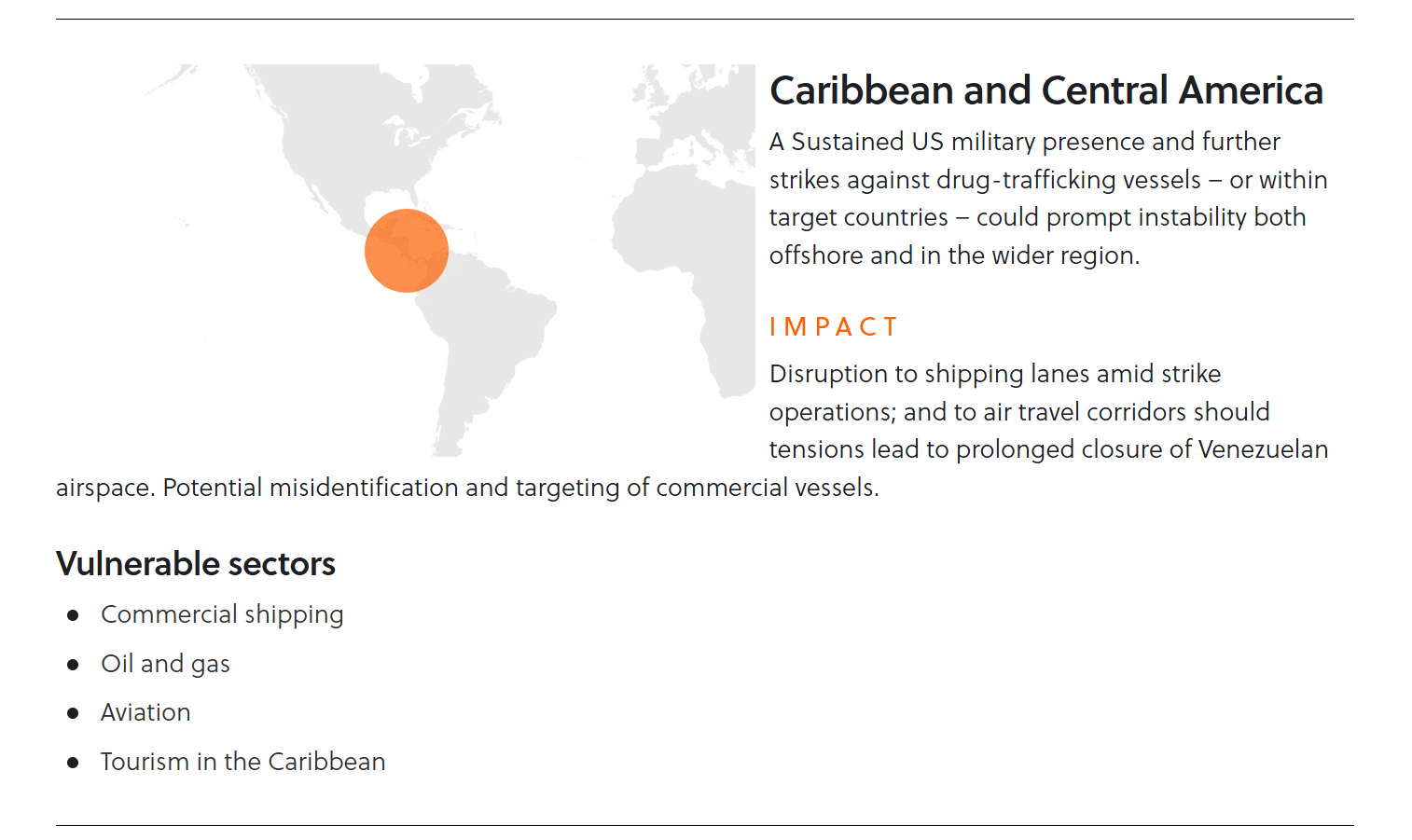

US actions in Venezuela and the wider Caribbean and eastern Pacific offer one of the clearest examples of how shifting priorities are shaping foreign and domestic policy. In its National Security Strategy (NSS), the administration identifies the Western Hemisphere as a primary theatre, arguing that US pre-eminence is essential to national security and prosperity. The strategy highlights border security, migration, drug trafficking and great-power competition as core vulnerabilities, calling for deployments to secure the border and combat cartels, and signalling willingness to use military force against designated “narco-terrorists” where deemed necessary.

Since August 2025, these priorities have driven a heightened focus on drug trafficking, which the White House casts as a national security crisis. The designation of several Latin American organised crime groups as Foreign Terrorist Organisations enabled the expanded use of military and counterterrorism tools, including a build-up of US assets and intensified air and maritime operations in the Caribbean and eastern Pacific. These operations culminated in air strikes on Caracas and the capture of Nicolás Maduro in January 2026. In the aftermath, President Trump stated that the US would “run Venezuela” until a “safe, proper and judicious transition” could be guaranteed. Beyond uncertainty over Venezuela’s long-term political stability, observers warn of potential retaliation by organised crime groups and militant actors such as the Colombia-based Ejército de Liberación Nacional (ELN). Furthermore, given China and Russia’s close political and economic ties to the former Maduro government and their likely efforts to offset an expanded US role in Venezuela and the wider hemisphere, there is potential for an escalation of wider geopolitical tensions.

Outlook

The designation of Latin American drug cartels as FTOs raises the stakes for companies with operations or counterparties in the region, since even unintended dealings that could be construed as providing ‘material support’ to an FTO may trigger serious legal, compliance, and reputational consequences.

Additionally, tourism‑dependent countries such as Jamaica worry that rising regional tensions could reduce visitor numbers, threatening the core of their economies. For instance, in November, President Trump warned that the “airspace above and surrounding Venezuela should be considered closed in its entirety”, prompting the US Federal Aviation Administration (FAA) to issue alerts to airlines operating in the area. Sustained military operations in the region are likely to exacerbate aviation disruptions and intensify concerns about travel to the wider region.

Maduro’s ouster is also likely to reshape Venezuela’s oil industry. With China accounting for nearly 80 percent of Venezuela’s oil exports prior to his capture, Washington prefers a future in which existing energy relationships pivot given its renewed focus on the Western Hemisphere. The US has announced a deal with interim President Delcy Rodríguez’s government to redirect USD 2 billion worth of crude to the US and expand the role of US oil companies in restructuring the sector. However, firms will face significant challenges, including deteriorated infrastructure, security risks, and unresolved legal disputes.

Critical minerals: The new frontier(s)

Economic stability and national security are now tightly linked to states’ ability to access critical minerals, required to support the energy transition, boost military-industrial development and economic growth, and secure geopolitical influence. Minerals like lithium, cobalt graphite and rare earths are central to batteries, advanced electronics and precision weapons systems, giving governments strong incentives to secure both raw materials and refining capacity. Competition has been particularly pronounced between the US and China, over access to key supply chains, where China dominates processing and refining capacity for many of these minerals, including much of the world’s graphite, cobalt and rare earths. Both powers increasingly frame critical minerals policy in national security terms, treating control over extraction and processing as strategic leverage in their broader rivalry.

To achieve this both countries have leveraged economic tools such as tariffs and export controls to protect domestic industries and gain bargaining power in this space. In 2025, for example, China introduced two waves of export controls on several rare earth elements including samarium and gadolinium, stating that exports to foreign countries have undermined its national security. The US is also taking a proactive approach to securing access to critical supply chains and strategic minerals. For example, in December 2025 it signed the Pax Silica declaration with Australia, Israel, Japan, Singapore and South Korea to offset China’s control of the sector by boosting cooperation in the areas of logistics, processing and advanced manufacturing. Europe, meanwhile, has adopted its own critical raw materials strategy and is increasingly seeking to diversify imports by deepening cooperation with “like-minded” resource-rich partners, expanding European extraction, and strengthening supply-chain resilience through measures such as stockpiling.

Outlook

Deposit-rich countries with significant untapped potential face both opportunities and challenges as they look to boost foreign investment in critical minerals. Many sought after deposits are located in already fragile or politically unstable states such as Bolivia, the Democratic Republic of Congo (DRC) and Ukraine, where governance constraints and security risks complicate large scale projects. Bolivia, for example, holds some of the world’s largest lithium reserves, but in 2025 has seen growing civil unrest and opposition from civil society and local activist groups over mining contracts with Chinese and Russian investors. Critics argue the agreements lack transparency and risk causing significant environmental damage. Meanwhile, Ukraine’s resource sector remains constrained by ongoing conflict, occupation of territory and infrastructure damage, limiting its ability to develop potential deposits and adding significant operational risk for investors. As this race intensifies, the impact on these countries – including intensified anti-mining sentiment, resource nationalism and fighting among state and non-state actors over supply chains – could aggravate existing instability, increasing political, security, and operational risks for investors and commercial operators.