The politics of money: US monetary policy direction in 2025 and its global ripple effect

Editor

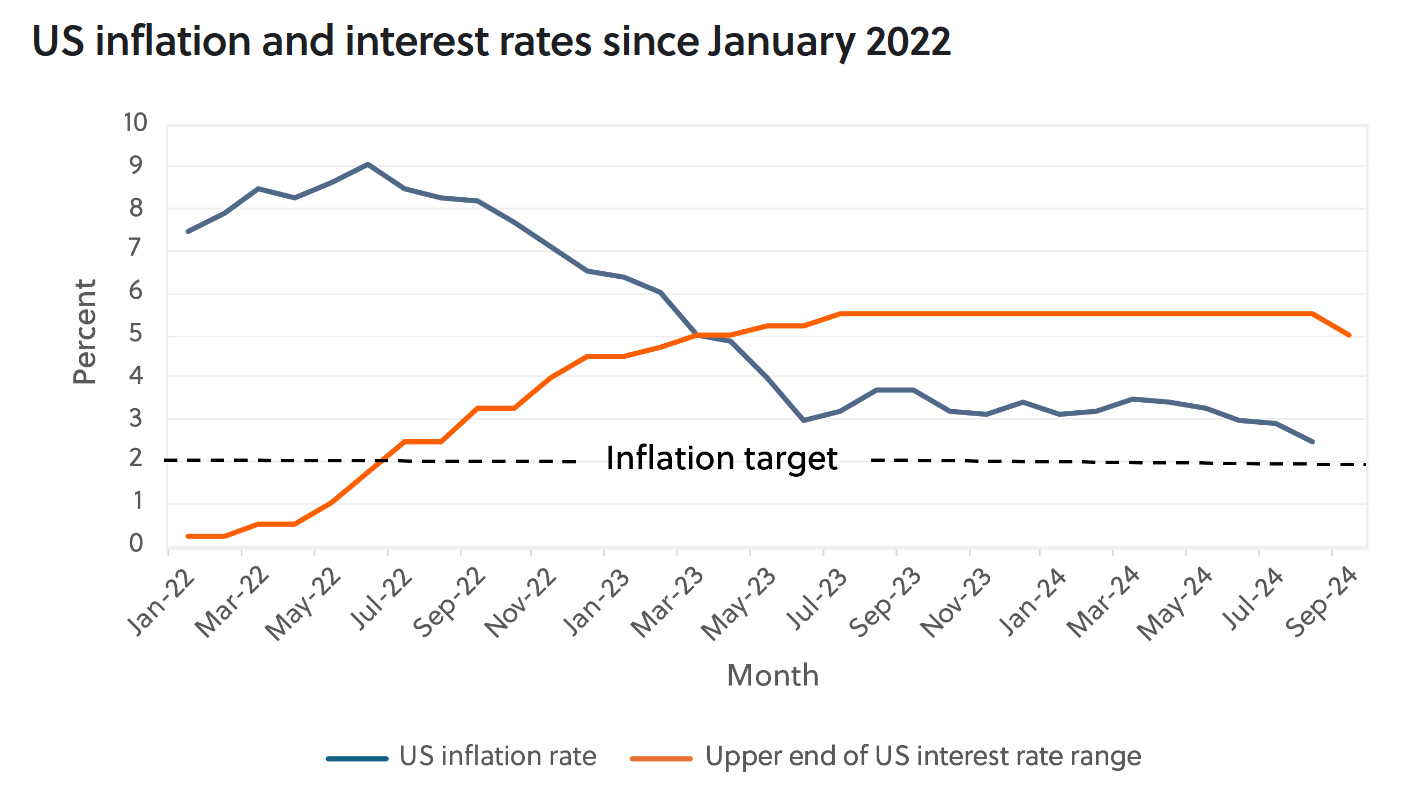

The US Federal Reserve has been in the spotlight since its long-foreshadowed interest rate cut in September – its first since 2020. With the US November election fast approaching, however, speculation is rife over whether a change in the presidency could halt – or even reverse – the US central bank’s widely anticipated strategy to gradually bring down interest rates over the coming years.

The mission of the Fed is to minimise inflation while simultaneously maximising employment, aimed at setting the US economy on a path of long-term growth, and it does this by adjusting interest rates. Decisions to raise borrowing costs are generally unpopular with voters, and therefore often frowned upon by politicians looking to win elections. The Fed, however, is a quasi-independent institution. While its governing body is appointed through political process – with a new Fed chair due to be appointed by the next president in 2026 – it nevertheless crafts its monetary policy independently of the political will in the legislative or executive branches of government. While control of US monetary policy sits squarely with the Fed, there are ways in which the economic policies of a sitting president can push prices higher or lower, and in this respect, we can expect vastly different approaches from a Kamala Harris or Donald Trump administration.

Harris and Trump’s differing approaches monetary policy

Harris’s economic proposals are organised around bringing living costs down for lower- and middle-income households – with proposals to lower healthcare costs, increase tax deductions for small businesses, and a proposed ban on what she terms retail price gouging. Her ability to implement such reforms to full effect, however, would depend heavily on the political composition of Congress. Harris has also pledged not to interfere with the Fed, should she enter the White House, and as such, barring any unforeseen external shocks, the Fed under Harris could be expected to continue its current strategy to bring interest rates down in the months to come.

By contrast, Trump has been openly critical of some of the decisions made by the Fed, beginning in 2018 during his first administration when the Fed increased interest rates four consecutive times. More recently, in August 2024, Trump suggested that he could drive increased economic growth if he were able to exert more political influence over interest rate decisions. Trump later walked the comments back. Should he win, Trump may put forward a candidate he favours as the next Fed chair in 2026, although such a nomination would still be subject to Senate approval. There are other checks and balances in place that limit the extent to which any president can influence the Fed. For instance, the Fed’s Board of Governors – the primary governing body of the Federal Reserve system – are politically appointed, but serve staggered 14-year terms, providing a measure of stability and continuity beyond four-year presidential administrations.

Ahead of the November election, Donald Trump’s campaign has promised a number of economic reforms that expand on his first-term policies, from import tariffs, to tax cuts for both personal and corporate income, to tightening migration controls. While some of these proposals, like reduced income taxes, may ease the cost of living, others could drive prices higher per some economists’ analysis. Expanding existing trade tariffs on imports, for instance, could increase the prices of some goods, particularly raw materials and intermediate products imported by factories, and those increases may be passed down to consumers. Additionally, mass deportations of undocumented workers – on the scale proposed by Trump – has the potential to increase labour costs for businesses. Policies such as these could drive fast economic growth, but they may also push prices up, and could prompt the Fed to shift its interest rate trajectory to counter the upward pressure on inflation.

While a range of local and global factors influence Africa’s macroeconomic outlook, a gradual easing cycle by the Fed would provide some relief to these economies.

The Fed’s impact on emerging economies

Although the Fed focuses on managing the US economy, its policies also have far-reaching effects on emerging markets, including those in Africa. In the coming year, African economies will hope the Fed continues its gradual easing cycle while offering clear guidance on its monetary policy to reduce uncertainty.

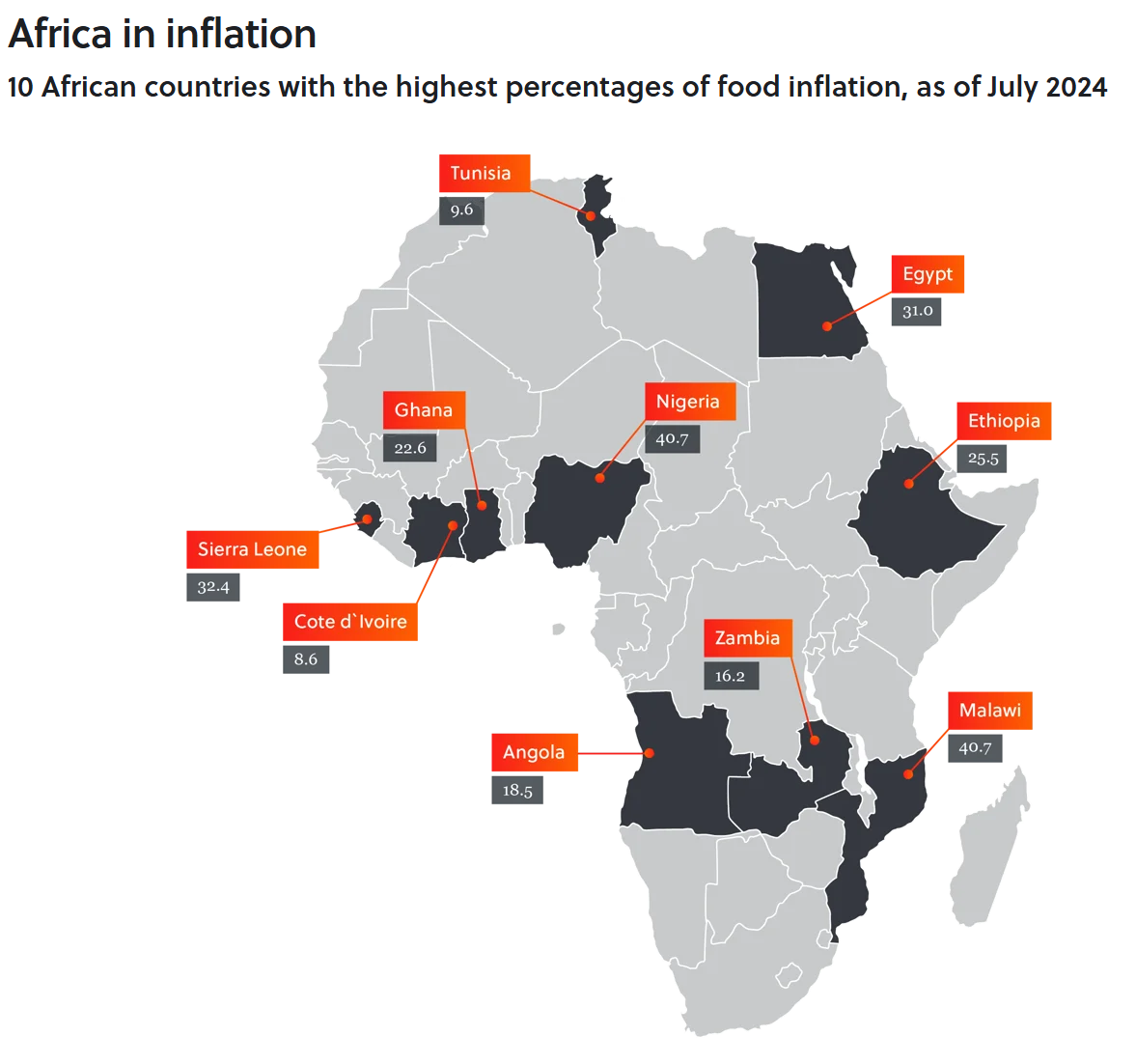

A steady path toward lower interest rates would benefit African economies by providing stable global financial conditions. Lower US interest rates tend to weaken the dollar, as investors move their capital into emerging markets seeking relatively higher returns. Dollar depreciation also provides some debt relief to economies with significant dollar-denominated debt. Currently, inflation in US and countries in Western Europe is approaching central banks’ two percent target, whereas it remains in double digits in nearly one third of African nations. There have been protests in recent months against rising costs of living, particularly food inflation, in several countries, including Ghana, Kenya, Nigeria, and Uganda. On 11 September, the Central Bank of West African States announced that it will keep its main interest rate at 3.50 percent, in place since December 2023, due to rising inflation. While a range of local and global factors influence Africa’s macroeconomic outlook, a gradual easing cycle by the Fed would provide some relief to these economies.

Alternatively, higher Fed rates usually attract capital inflows and strengthen the dollar, increasing import costs and dollar-denominated debt burdens for African countries. In 2022, for example, after the Fed’s seven rate hikes strengthened the dollar, Sierra Leone experienced inflation surpassing 20 percent, national currency depreciation, and increased debt servicing costs. In August 2022, protests broke out over rising costs of living, leaving at least 33 people dead.

Wider trade-related concerns

Monetary issues aside, African countries are concerned about the impact of certain trade policies, such as Trump’s proposed 60-percent tariffs on Chinese imports, and 10-20 percent tariffs on other imports. During his first term, Trump introduced tariffs primarily targeting major trade partners like China, the EU, Canada, and Mexico. There were limited tariffs on several South African steel and aluminium products, although uncertainty in the global economy had an indirect impact on Africa, such as a drop in commodity prices, large stock exchanges and national currencies. Several international financial organisations, such as the International Monetary Fund (IMF) and African Development Bank, reduced growth forecasts for certain African countries with significant exposure to China, which experienced an economic slowdown in 2018-19. This is due to China’s status as Africa’s largest bilateral trade partner, with the IMF saying in late 2023 that “a one percentage point decline in China’s growth rate could reduce average growth in the [sub-Saharan African] region by about 0.25 percentage points within a year.”

However, Trump is not the only candidate proposing new tariffs, as Harris too has called for “targeted and strategic tariffs” to support American workers, continuing a pro-tariff shift begun under President Joe Biden’s administration. Biden continued most of the tariffs on China from Trump’s first term and introduced new ones, such as 100 percent tariffs on electric vehicles; 50 percent on solar cells; and 25 percent on electric vehicle batteries, critical minerals, steel, aluminium, face masks and ship-to-shore cranes.

Importantly, the impact of US-China trade war is not entirely negative for Africa. Mutual US-China tariffs and related reduction in bilateral trade can create opportunities for African countries to increase exports to the US and China. According to one academic study published in December 2013, the US-China trade war may have had a negative impact on mineral, metal and service sectors in Africa, but there was growth for agriculture, food and oil and gas industries. Proactive policymaking from African countries can allow them to take advantage of US-China decoupling in the same way as other middle income countries, such as Vietnam, India, Mexico, and Malaysia.

While control of US monetary policy sits squarely with the Fed, there are ways in which the economic policies of a sitting president can push prices higher or lower.

All eyes on the US

With the US dollar remaining the world’s reserve currency for the foreseeable future, global trade prices and currency fluctuations will remain underpinned by monetary shifts in the US, with significant consequences for emerging economies. As such, the upcoming US election and the economic policies of the next administration will have far-reaching consequences, not only for the monetary policy of the Fed, but for central banks the world over. Borrowers across the globe may have breathed a sigh of relief after the Fed cut interest rates in September, but that trajectory could easily shift depending on the actions of the next US president.